Risk-on Sentiment

Reshoring Revival of U.S. Manufacturing

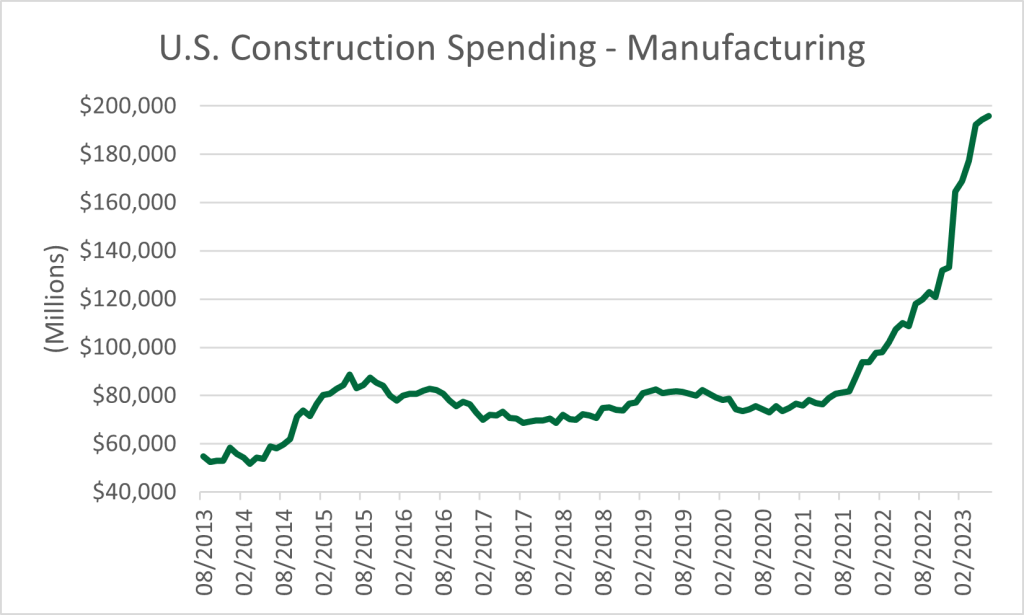

Overall manufacturing indicators have shown signs of slowing, but that hasn’t stopped U.S. corporations from looking ahead. Construction spending on manufacturing facilities has seen a revival over the past three years. From September 2020 through May 2023, construction spending on manufacturing facilities increased from $73 billion to $194 billion. This is small relative to the U.S. economy, but nonetheless a meaningful trend. Specifically, new construction spending has been concentrated in advanced manufacturing of computer, electronic, and electrical facilities. Government subsidies have helped, but growth accelerated well before the announcement of the Inflation Reduction Act. Reshoring (companies relocating manufacturing to the U.S.) of manufacturing can be somewhat attributed to supply chain diversification post-COVID. The number of companies announcing reshoring and increased domestic production has nearly doubled over the past three years.

China Slowdown

Economic momentum in China is facing headwinds. Second-quarter economic growth expanded only 6.3% year-over-year, as quarter-over-quarter growth slowed to 0.8% from 2.2% in the first quarter. Weaker domestic and global demand were two significant factors to the slowdown. Exports declined double digits, continuing a weaker trend from earlier this year. A falling consumption trajectory has followed declining personal income growth. China’s leadership acknowledged insufficient domestic demand, signaling proactive future fiscal and monetary policy.

Bonds: Riskiest Bonds Outperform

Overall bond market performance declined last month, but the riskier bond components followed equity trends. The U.S. Treasury Index declined -0.35% last month, as the Bloomberg U.S. Corporate Index (investment grade bonds) advanced +0.34% and Bloomberg U.S. Corporate High Yield Index increased +1.38%. Investors took comfort with the economic trajectory, willing to seek bonds with more risky profiles in exchange for higher relative interest rates. Since the end of March, the interest rate from a high yield bond relative to a Treasury narrowed nearly 1.50%, underscoring the shift in risk sentiment.

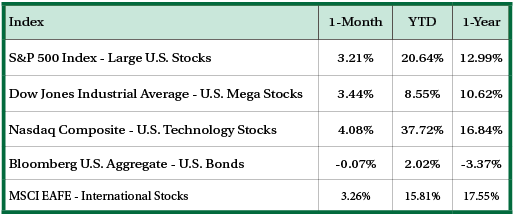

Equities: Nine straight years of gains in July

The market advanced in the month of July for the ninth consecutive year. The specific components behind the risk-on sentiment for equities differed slightly from the drivers year-to-date. Mega-capitalization, technology companies were responsible for performance this year, however small-capitalization equities took the lead in July. While small-cap equities are riskier given limited business diversification, improving economic sentiment tends to be supportive. In addition, small-caps are inexpensive relative to large-cap equities and are exhibiting an improvement in growth as earnings revisions have increased over the past three months.

Federal Reserve hikes rates by 0.25%

The Federal Reserve (Fed) raised its benchmark rate to a range of 5.25%-5.50%, the 11th rate increase since March 2022. Fed Chair Jay Powell noted future monetary policy will be “data dependent,” waiting for clarity on incoming economic data before committing to a policy course. Market participants share the viewpoint of near-term economic opaqueness with the Fed, expecting rates to be held steady over the next couple of months and a 40% possibility of another 0.25% hike at the beginning of November. Policymakers’ wait-and-see approach is possible because of calm capital markets and the inflation rate trending towards its long-term target.

Although we believe it to be reliable as of the publication date and have sought to take reasonable care in its preparation, all information provided is FOR INFORMATIONAL PURPOSES ONLY and we make no representations or warranties regarding its accuracy, reliability, or completeness and assume no duty to make any updates in the event of future changes. Past performance may not be indicative of future market results. Any examples used (including specific securities) are generic and meant for illustration purposes only and are not, and should not be interpreted as, offers to buy or sell such securities. To the extent indices are referenced, please note that you are not able to invest directly in an index.

Nicolet Wealth Management is a brand name that refers to Nicolet National Bank and certain of its departments and affiliates that provide investment advisory, trust, retirement planning and insurance services. Investment advisory services offered through Nicolet Advisory Services, LLC (dba Nicolet Wealth Management), a registered investment advisor.

All investments are subject to risks, including possible loss of principal, and are: NOT FDIC INSURED; NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; AND NEITHER DEPOSITS OR OTHER OBLIGATIONS OF, NOR GUARANTEED BY, Nicolet National Bank or any of its affiliates. Neither Nicolet Advisory Services nor its affiliates offer tax or legal advice. You should consult with your legal and tax professionals before making investment decisions.