U.S. Consumer Demand Fueled Growth

Global Stocks Unable to Sidestep Headwinds

A late month decline in stocks rekindled the downward trend since early August, as rates returned to the forefront of investors’ minds. The S&P 500 index, a proxy for U.S. large-cap equities, closed in correction territory (down 10% or more from its near-term peak), following the lead of international stock weakness. In fact, the stock market has been on shaky ground for most of the year on few stocks participating in the rally, underlying cautious leadership (stocks less tied to the economy leading gains) and weaker earnings revision momentum. First, performance this year has been led by only a handful of stocks (10 largest weighted stocks in the S&P 500 index have contributed 134% of YTD gains), reinforcing lack of confidence. Second, quality stocks with low earnings volatility and the biggest companies with diverse sources of earnings have led the market. Finally, earnings revisions are unsettled and no longer a tailwind for the market.

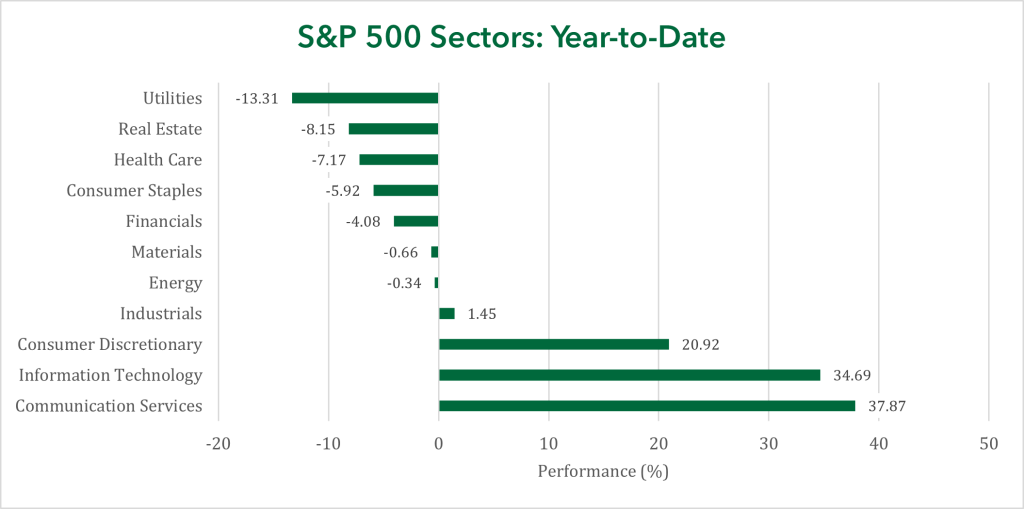

Sector Reversal

After exhibiting weakness in the third quarter of 2023, the information technology sector regained leadership. Historically, rising interest rates are a headwind for this sector as better bond investment opportunities become available and future earnings of technology are less valuable. While that sentiment remains true, investors have found greater comfort in high cash technology companies amidst economic and geopolitical uncertainty. For example, Apple Inc. (AAPL) has $166 billion in cash (as of Q3 2023) that could be invested at a relatively high interest rate compared to recent history, on top of a strong core business.

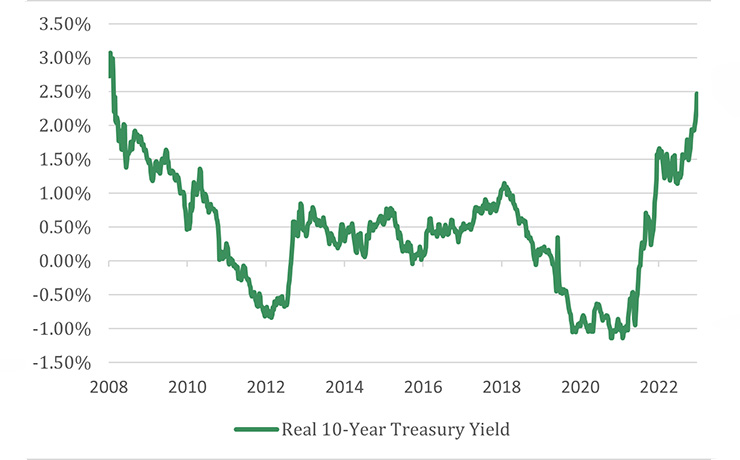

Interest Rates Take Another Step

Consistent with the trading pattern since May 2023, Treasuries saw yields rise in October. The 10-year Treasury yield advanced from 4.57% to 4.93%, the 30-year Treasury increased above 5%, and even the 3-year Treasury yield advanced 0.13%. However, as the calendar nears an end for the year, the rise in yields has been concentrated with longer-term maturities, while short-term maturities have remained stable. For example, the difference between a 2-year Treasury yield and the 10-year Treasury yield steepened nearly 0.30%. Much of this increase can be attributed to investors’ required compensation for holding long maturity bonds, as the unknown clouds long-term investments. The increased compensation reflects views on the economy, increased Treasury issuance and overall heightened rate risk.

Rising Oil Prices

Middle East conflict typically reintroduces uncertainty to oil markets. International and U.S. oil benchmarks declined about 8% and 11% in October, respectively, but most of the losses occurred prior to the October 7th outbreak of the Israel-Palestine conflict. However, oil prices have fluctuated daily as investors try to grasp the severity to bordering oil producing nations and the risk of a wider conflict. From a U.S. perspective, upward gasoline price shocks are certainly a risk to consumers, but shocks are no longer as damaging to the broad U.S. economy because of oil production self-sufficiency. The U.S. has become a net exporter of petroleum products.

Consumption Supporting U.S. Growth

Consumer spending has been able to withstand higher borrowing costs this year, confirmed again by the first estimate of growth for the third quarter 2023. The U.S. economy advanced by 4.9% quarter over quarter, reinforced by consumer spending increasing more than 4% (the most since 2021), government expenditures rising consistently and a boost from private investment. Spending was concentrated in sporting equipment, travel, and home furnishing, partially supported by increased income and the balance coming from reduced savings (personal saving as a percentage of disposable income fell 1.5% last quarter). The lack of a savings tailwind and higher interest rates question the sustainability of a strong spending contribution to the economy.

Although we believe it to be reliable as of the publication date and have sought to take reasonable care in its preparation, all information provided is for informational purposes only and we make no representations or warranties regarding its accuracy, reliability, or completeness and assume no duty to make any updates in the event of future changes. Past performance may not be indicative of future market results. Any examples used (including specific securities) are generic and meant for illustration purposes only and are not, and should not be interpreted as, offers to buy or sell such securities. To the extent indices are referenced, please note that you are not able to invest directly in an index.

Nicolet Wealth Management is a brand name that refers to Nicolet National Bank and certain of its departments and affiliates that provide investment advisory, trust, retirement planning and insurance services. Investment advisory services offered through Nicolet Advisory Services, LLC (dba Nicolet Wealth Management), a registered investment advisor. Securities offered through Private Client Services, LLC (“PCS”), member FINRA/SIPC. PCS is not affiliated with Nicolet National Bank or Nicolet Wealth Management.

All investments are subject to risks, including possible loss of principal, and are: NOT FDIC INSURED; NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; AND NEITHER DEPOSITS OR OTHER OBLIGATIONS OF, NOR GUARANTEED BY, Nicolet National Bank or affiliates.