Nicolet Wealth Management Monthly Newsletter 2.2.24

Economic Activity Shows Resilience

U.S. economic activity continues to defy expectations, as U.S. real GDP advanced 3.3% annualized in the 4th quarter, the sixth consecutive quarter above 2%. Growth slowed from 3rd quarter’s pace of 4.9%, but topped the consensus estimate of 2%. Once again, consumer spending accounted for the bulk of growth, rising 2.8% on healthcare services, food services and nondurables. Consumers also spent on residential investment, as growth has been concentrated in new home construction. However, the upside surprise was driven by trade activity adding nearly 0.50% to headline growth and government spending. For the full year 2023, the U.S. economy expanded 3.1%, up from 0.7% a year earlier.

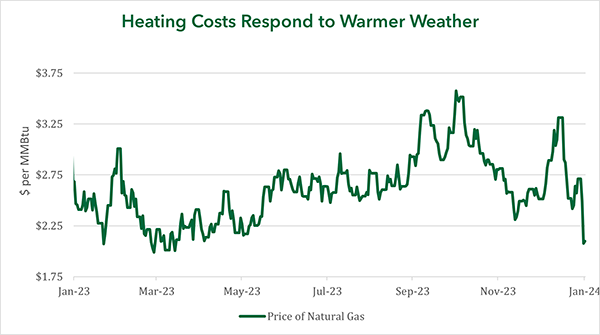

Home Heating Costs Contained

Early January’s polar vortex sent natural gas prices higher, but a combination of larger stockpiles and warmer weather has eliminated the winter premium most expect at this time of the year. Despite the third-largest withdrawal ever from natural gas storage facilities, stockpiles remain 5.2% above the five-year average. Forecasts of warmer-than-expected weather into February has shifted gas stockpiles to remain abundant. Natural gas prices topped out around $3.31 MMBtu mid-January, declining to about $2.10 MMBtu to end the month.

Q4 2023 Earnings Season Kicks Off

Investors are looking for confirmation that company earnings are matching the resilience of the economy. So far, earnings growth is almost doubling expectations from a few weeks ago at 2.3% versus a year ago. Financials, consumer staples and industrials sectors have reversed early expectations of a decline, as nearly 80% are reporting higher earnings than estimates (above the near- and long-term average). Most notably, revenue has been the catalyst of better results, contrary to initial expectations of cost cutting propelling earnings growth. Technology remains the bellwether for the stock market, as earnings expectations have steadily increased over the last 3 months, while earnings for the rest of the market have dropped. Putting this into context, technology earnings growth is expected to be 16% year-over-year, up from a 2% year-over-year contraction just six months ago.

Mega-cap Stocks Take the Lead Again

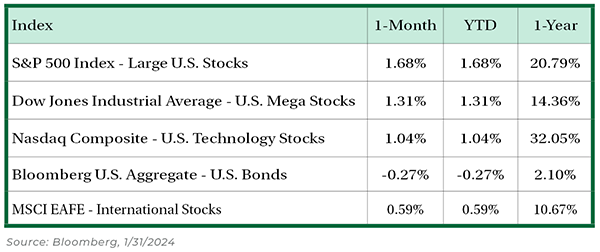

Stocks reverted back to its 2023 trend after a brief burst in performance from small-caps late in the year. The S&P 500 index (large-cap stocks) returned 1.7% in January, topping performance of the Russell mid-cap index and the Russell 2000 index (small-cap stocks) of -1.4% and -3.9%, respectively. There are a few explanations for the performance dispersion, but a reversal higher in the 10-year Treasury yield for most of the month was the impetus. The technology, communication services, and healthcare sectors showed the ability last year to withstand higher interest rates. This year’s move in the 10-year Treasury yield (+0.3% from peak to trough) pales in comparison to last year’s 1.7% increase from peak to trough, although it is still notable that investors are finding solace in growth stocks during an upward advance in rates.

Federal Reserve’s Slow Pivot

The January Federal Open Market Committee (FOMC) meeting, where Federal Reserve (Fed) members determine the appropriate stance of monetary policy, ended with the benchmark rate in a 5.25%-5.5% target range, unchanged from December. Most notable in the FOMC statement, a new reference was made with the Fed considering “any adjustments” to the benchmark rate from a previous bias towards a potential hike. Also, Fed chair Jay Powell noted that rates are at their peak for this cycle during the scheduled press conference. Despite the Fed’s preference for a slow pivot from tighter monetary conditions as inflation remains above target, investors still expect a 35% chance of a 0.25% rate cut in March.

Although we believe it to be reliable as of the publication date and have sought to take reasonable care in its preparation, all information provided is FOR INFORMATIONAL PURPOSES ONLY and we make no representations or warranties regarding its accuracy, reliability, or completeness and assume no duty to make any updates in the event of future changes. Past performance may not be indicative of future market results. Any examples used (including specific securities) are generic and meant for illustration purposes only and are not, and should not be interpreted as, offers to buy or sell such securities. To the extent indices are referenced, please note that you are not able to invest directly in an index.

Nicolet Wealth Management is a brand name that refers to Nicolet National Bank and certain of its departments and affiliates that provide investment advisory, trust, retirement planning and insurance services. Investment advisory services offered through Nicolet Advisory Services, LLC (dba Nicolet Wealth Management), a registered investment advisor.

All investments are subject to risks, including possible loss of principal, and are: NOT FDIC INSURED; NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; AND NEITHER DEPOSITS OR OTHER OBLIGATIONS OF, NOR GUARANTEED BY, Nicolet National Bank or any of its affiliates. Neither Nicolet Advisory Services nor its affiliates offer tax or legal advice. You should consult with your legal and tax professionals before making investment decisions.