Software on Sale

A sell-off in software stocks took another step lower in February, as investors reassessed the extreme prices placed on investments relying on artificial intelligence (AI) advancements. The S&P 500 software index, which represents the largest software companies, declined nearly 24% at the lowest point in February to begin the year. The main catalyst for this sharp sell-off to start the year is investor skepticism over AI technology spending and its commensurate return. The top technology companies in the S&P 500 are expected to spend more than $646 billion in 2026. Market history tells us that companies spending this much on building operating capacity typically have lower forward returns.

Manufacturing Surges

The ISM Manufacturing PMI, a snapshot of U.S. industrial activity, entered expansionary territory for the first time in 12 months, with rising demand for orders forcing factories to increase production to meet demand. The overall manufacturing PMI surged to 52.6 in January from 47.9 in December as the new-orders sub-index advanced to 57.1. Demand-side factors have contributed to the upside, with new export orders and the order backlog both increasing. Weakness in manufacturing has been a massive headwind to U.S. economic growth, while the services segment of the economy has carried growth for the past couple of years. A turnaround in the manufacturing segment would be an indicator of U.S. economic stability.

Payroll Growth Stabilizes

U.S. employers added 130,000 jobs in January 2026, the most in more than a year, while the unemployment rate declined to 4.3%. An acceleration in hiring was led by healthcare, which has added the most jobs since 2020 and led payroll growth in 2025. Other segments of the economy adding jobs in the first month of the year include construction and professional and business services. Manufacturing exhibited the first monthly gain in employment in more than a year. Pockets of the jobs data confirm the better manufacturing activity underlined in the PMI data from earlier in the month.

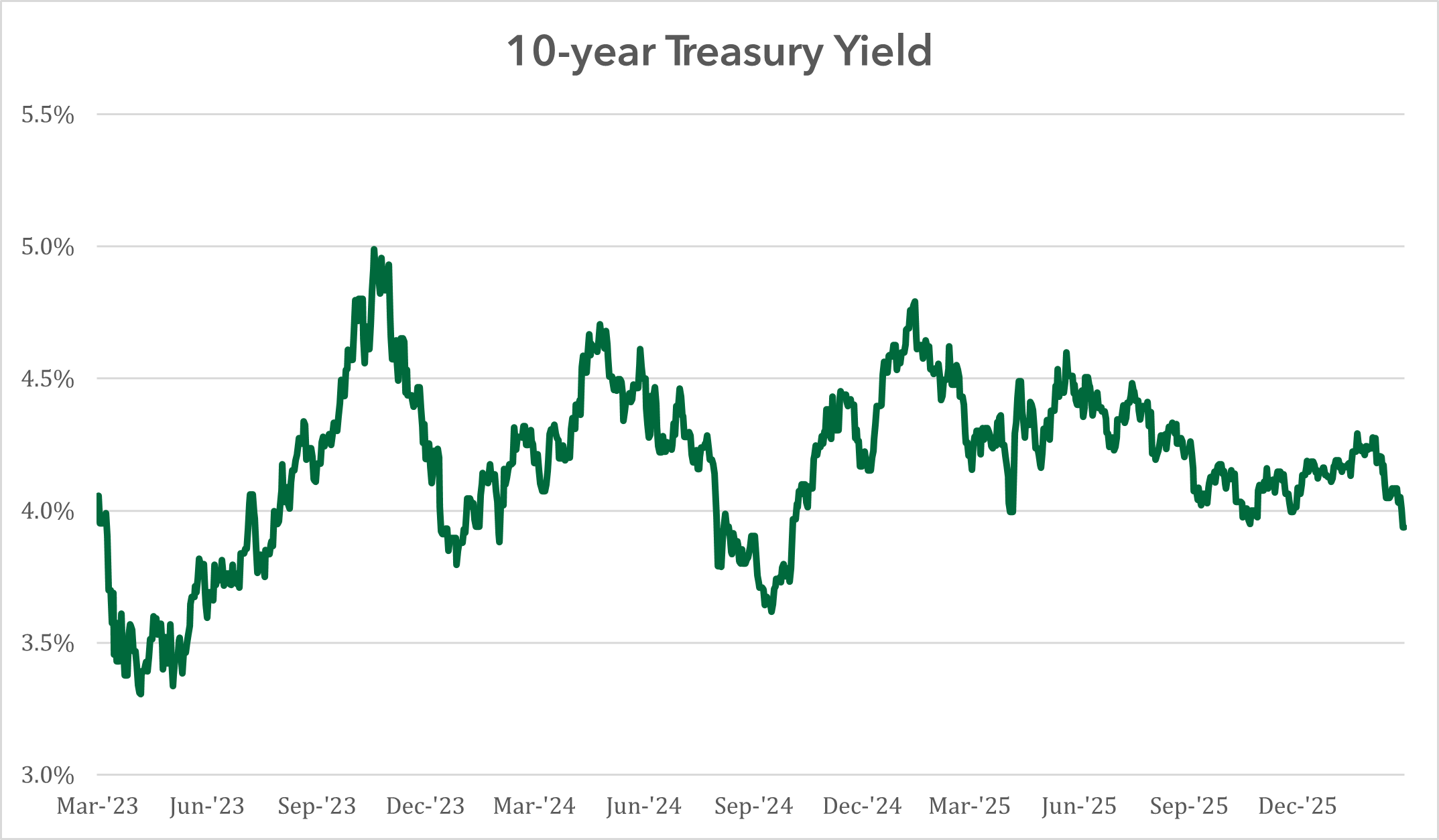

Rate Reversal

Investors sought the safety of Treasury bonds in February, as the 10-year Treasury yield fell below 4% for the first time since November 2025, sparking a rally in U.S. bonds. The Bloomberg Aggregate bond index advanced 1.6% in February, which was the best return since July 2024. The main catalyst behind the move in rates was rising geopolitical tensions, but also taking the headlines was growing concerns over artificial technology’s long-term effect on labor market growth. The 30-year Treasury yield’s decline was even more prominent, dropping from 4.9% to 4.6% in a matter of one month.

Stocks Go International

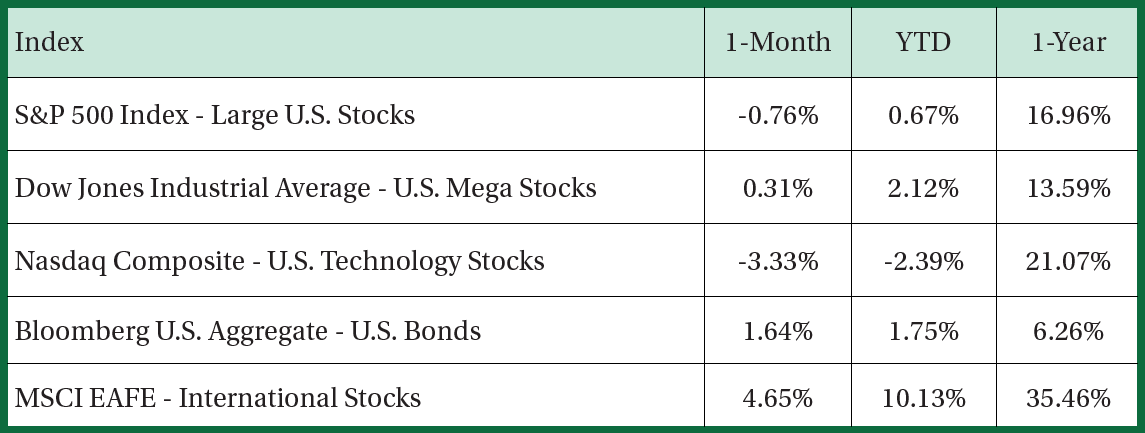

Consistent with the first month of the year, international stocks led global markets on a strong rally from emerging stocks. The MSCI Emerging Market Index advanced 5.5%, as the asset class continues to find support from better growth revisions and relative cheapness to the global markets. Not far behind were international developed stocks, which advanced 4.6% last month. International developed stocks have higher dividend yields, which investors look to substitute during periods of global rate declines. MSCI EAFE Index, a representation of international developed stocks, has a dividend yield of 3.28%, while the S&P 500 index only has a dividend yield of 1.18%.

Although we believe it to be reliable as of the publication date and have sought to take reasonable care in its preparation, all information provided is FOR INFORMATIONAL PURPOSES ONLY and we make no representations or warranties regarding its accuracy, reliability, or completeness and assume no duty to make any updates in the event of future changes. Past performance may not be indicative of future market results. Any examples used (including specific securities) are generic and meant for illustration purposes only and are not, and should not be interpreted as, offers to buy or sell such securities. To the extent indices are referenced, please note that you are not able to invest directly in an index.

Nicolet Wealth Management is a brand name that refers to Nicolet National Bank and certain of its departments and affiliates that provide investment advisory, trust, retirement plan level services, and insurance services. Investment advisory services offered through Nicolet Advisory Services, LLC (dba Nicolet Wealth Management), a registered investment advisor.

All investments are subject to risks, including possible loss of principal, and are: NOT FDIC INSURED; NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; AND NEITHER DEPOSITS OR OTHER OBLIGATIONS OF, NOR GUARANTEED BY, Nicolet National Bank or any of its affiliates. Neither Nicolet Advisory Services nor its affiliates offer tax or legal advice. You should consult with your legal and tax professionals before making investment decisions.

Listen & Subscribe to our Podcast

Tune in for the next episode, subscribe or follow us wherever you listen to podcasts.